Alternative Credit Risk Management & Assessment Guide

Introduction

What is Credit Risk Management and Assessment?

Key Credit Risk Assessment Methods Used by Financial Institutions

What is Alternative Credit Risk Scoring?

Why Alternative Credit Risk Scoring Matters

When is Alternative Credit Risk Scoring Necessary?

What Are the Main Types of Alternative Credit Data?

How Is Alternative Credit Data Applied in Credit Risk Scoring?

Best Practices for Collecting Alternative Data for Credit Scoring

Important Considerations When Using Alternative Credit Data

Regulatory Compliance in Credit Risk Scoring

Understanding the Types of Credit Risk and Scoring Factors

Traditional vs Alternative Credit Risk Scoring Models

The Credolab’s Credit Risk Scoring Process Explained

How AI/Machine Learning is Improving Credit Risk Scoring

Credit Risk Score Calculation Example

How Credit Risk Analytics Platforms Support Risk Teams

Benefits of Using Alternative Data in Credit Risk Scoring

Best Practices for Effective Credit Risk Scoring and Management

The Business Impact of Smarter Credit Risk Scoring

How Can Credolab Help with Credit Risk Assessment?

Conclusion

FAQs

Introduction

Credit risk management and assessment are vital practices for financial institutions to evaluate and reduce the risk of borrower default. These processes involve using a combination of traditional credit data alongside innovative alternative data models to make well-informed lending decisions.

Advances in machine learning, or ML, and artificial intelligence, or AI, are transforming credit scoring, enabling faster, more accurate, and adaptive risk evaluations. Furthermore, alternative credit risk scoring plays a crucial role in expanding financial access to underserved populations by integrating diverse alternative data sources.

This guide explains credit risk management and assessment and explores key traditional and modern credit scoring methods. It also highlights the role of alternative data and machine learning, and outlines best practices and challenges in credit risk decision-making.

What is Credit Risk Management and Assessment?

Credit risk management and assessment are structured practices employed by financial institutions to evaluate and mitigate the risk of borrower default.

The credit risk management process refers to monitoring, controlling, and mitigating risks after lending decisions are made.

However, credit risk assessment involves the initial evaluation of a borrower’s creditworthiness using data and scoring models. It is a critical step to decide on loan approvals.

Together, these two functions are essential to safeguard the institution’s financial stability and optimise lending processes with informed risk-based decisions.

Key Credit Risk Assessment Methods Used by Financial Institutions

Financial institutions utilise a range of key credit risk assessment methods, including traditional and modern approaches, to accurately evaluate borrower creditworthiness.

Traditional Methods

Traditional methods largely rely on classic, linear scorecard models. Scorecards use historical credit bureau data and financial information to assign a credit score. This score predicts the likelihood of default.

Behavioural analysis builds on this by tracking a borrower's actual behaviour over time, such as payment patterns and credit utilisation. These methods, while effective, often face limitations in assessing thin-file or no-file customers.

Modern Risk Assessment Methods

Modern risk assessment methods incorporate machine learning models. These models analyse large volumes of diverse data to identify complex patterns predicting credit risk better than traditional techniques.

Machine learning can adapt and improve over time, making assessments more dynamic and robust. This adaptability allows for real-time credit risk updates based on new data.

Furthermore, machine learning models can detect subtle risk factors that human analysts might miss, enhancing prediction accuracy.

Alternative Data Models

Alternative data models are increasingly incorporating more complex machine learning into scorecard models. They leverage traditional and alternative data sources, including utility payments, rental history, mobile phone usage, and social media activity. These models identify non-linear patterns that predict credit risk with often greater accuracy.

This approach broadens financial inclusion by enabling lending decisions for those with limited traditional credit history. Moreover, alternative data helps reduce bias inherent in traditional data sources.

What is Alternative Credit Risk Scoring?

Alternative credit risk scoring is a methodology that employs alternative data to evaluate a borrower's creditworthiness.

It is the practical application of using alternative data and models to generate credit scores for individuals who may not have sufficient traditional credit data. This scoring method leverages alternative data models, enabling lenders to evaluate credit risk in underserved or thin-file populations.

By analysing these diverse data points, alternative credit scoring creates a more comprehensive and nuanced financial profile. It benefits borrowers who are “credit invisible” or have thin credit files, such as young adults, immigrants, or those in cash-based economies.

Additionally, alternative scoring uses advanced algorithms and machine learning to detect patterns in behaviour and device usage, which supports better risk assessment and fraud detection.

Why Alternative Credit Risk Scoring Matters

First, alternative credit risk scoring matters because it significantly increases the predictive power of credit assessments.

By incorporating diverse, alternative data sources such as device behaviour, utility payments, and online activity, it creates a deeper insight into borrower behaviour beyond what traditional credit data can offer.

This leads to more accurate predictions of repayment ability, reducing default rates and enhancing portfolio stability.

Second, this method plays a critical role in expanding financial inclusion. Many individuals, such as young adults, immigrants, and those in underbanked regions, lack traditional credit histories.

Finally, alternative credit scoring modernises risk assessment by delivering dynamic, real-time insights. Unlike static historical scores, it adjusts quickly to changing borrower behaviour and market conditions. By analysing real-time data signals that reflect current financial health, this responsiveness improves decision-making speed and accuracy in fast-moving digital financial environments.

When is Alternative Credit Risk Scoring Necessary?

Alternative credit risk scoring is necessary when traditional credit data is incomplete or absent. This situation commonly affects thin-file or no-file customers who lack extensive credit histories.

It also applies to underbanked and underserved populations, including immigrants and individuals in cash-based economies. These groups face barriers in accessing credit due to data gaps and information asymmetry in traditional models.

In a digital lending environment, the issue of data gaps and information asymmetry is exacerbated because smartphones have become a norm, especially among no-file customers and underbanked or underserved populations.

These groups heavily rely on mobile devices for financial activities, social interactions, and everyday communication, generating vast amounts of valuable behavioural data.

However, smartphone ubiquity also means lenders face challenges related to data privacy, regulatory compliance, and ethical usage of this sensitive information.

Consequently, the widespread use of smartphones amplifies the need to address information imbalances while ensuring responsible and ethically rich data handling.

What Are the Main Types of Alternative Credit Data?

Alternative credit data provides lenders with insights beyond traditional credit reports to better assess creditworthiness. The main types include:

Behavioural Biometrics and Metadata

How users interact with digital platforms, such as typing speed, mouse movements, and navigation patterns. These behavioural signals help detect fraud and assess borrower consistency and reliability.

Telco Data

Mobile phone usage records, including call and text patterns, prepaid top-ups, and mobile money transactions. Consistent data patterns can reflect financial discipline and stability, especially in underbanked populations.

Device Metadata

Information about the borrower’s device, such as device type, operating system, location data, and IP address changes. Leveraging device data helps verify identity and detect suspicious behaviour.

Utility Payment History

Payment records for services like electricity, gas, water, and internet. A strong history of timely utility payments demonstrates financial responsibility and a capacity for repayment.

App Usage Data

Usage patterns from financial and non-financial apps can reveal behavioural traits relevant to credit risk, such as punctuality in bill payments and spending habits.

Together, these alternative data sources provide a more comprehensive picture of financial behaviour, improving credit scoring accuracy and expanding lending opportunities to individuals lacking traditional credit histories.

How Is Alternative Credit Data Applied in Credit Risk Scoring?

Financial institutions apply alternative credit data in credit risk scoring by integrating it into their credit risk scoring models, used either as standalone signals or as enhancements to traditional credit scores.

This integration begins by identifying relevant alternative data sources, such as utility payments, rental history, device metadata, and behavioural patterns. These data points are then cleansed, validated, and mapped to the institution’s existing credit frameworks.

In practice, alternative data can be used to develop new standalone credit scores for borrowers lacking traditional credit histories. These models assess creditworthiness using behavioural and transactional insights to predict repayment ability.

Alternatively, institutions may enhance traditional credit scoring models by supplementing bureau data with alternative signals, which improves predictive accuracy and reduces default risks.

For example, some fintech lenders offer instant personal loans by analysing mobile phone metadata and app usage patterns. Another instance involves lenders who utilise rental and utility payment data to approve credit for thin-file customers.

Additionally, lenders in emerging markets who use alternative data, such as telco data and digital footprints, provide loans to unbanked populations and assess risk.

Best Practices for Collecting Alternative Data for Credit Scoring

Ethics

- Responsible and transparent data use

- Fair and ethical credit assessment

- Avoids bias and misuse

- Strong governance and oversight

- Regular audits to uphold standards

Privacy

- Data anonymisation and pseudonymisation

- Clear explanation of data usageGDPR, CCPA, PDPA Compliant

- Secure processing of behavioural and device metadata

- Data minimisation (collect only what is necessary)

User Consent

- Clear, informed, and explicit user permission

- Transparent access and usage details

- SDK-based collection with user consent

- App-level permission management for users

- Privacy-centred, permission-driven data journey

The best practices for alternative data collection in credit scoring are built on prioritising ethics, privacy and user consent.

Financial institutions must obtain clear, informed consent from users before accessing any personal or behavioural data. Transparency about what data is collected, how it will be used, and who will access it builds trust and ensures compliance with privacy regulations like GDPR and CCPA.

One common and efficient data collection approach is the use of Software Development Kits (SDKs) integrated into mobile applications. SDKs enable seamless, real-time capture of relevant alternative data, such as behavioural biometrics and app usage, directly from users' devices with their permission. This method reduces manual errors and enhances data accuracy.

App-based collection offers control and convenience for users, allowing them to manage permissions and data sharing preferences easily. This fosters an ethical relationship by placing users at the centre of their data journey.

Anonymisation is critical to protect user privacy. Data should be de-identified or pseudonymised to prevent any back-tracing to individuals while preserving its analytical value. This technique mitigates risks of identity theft and misuse.

Furthermore, data minimisation principles should be followed, collecting only strictly necessary information for credit assessment. Regular audits and monitoring are essential to proactively uphold ethical standards and regulatory requirements

Important Considerations When Using Alternative Credit Data

When using alternative credit data, several important considerations must be addressed to ensure responsible and effective credit risk management.

Compliance with privacy regulations, such as the General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA), are non-negotiable.

Institutions must secure explicit user consent, provide transparency about data collection, and allow users to exercise their rights, including data access and deletion, as outlined in privacy policies. Failure to comply can result in severe legal penalties and damage to an institution’s reputation.

Data quality is another critical factor. Alternative data must be accurate, reliable, and relevant to credit risk assessment. Poor-quality data can lead to erroneous credit decisions and increase default risk.

Continuous data validation and cleansing mechanisms are essential to maintain integrity. Implementing robust data governance frameworks helps maintain consistent data quality over time.

Model fairness is vital to prevent bias or discrimination across any borrower groups. Institutions should regularly audit credit models to ensure equitable treatment and mitigate adverse impacts on vulnerable populations. Using explainable AI (XAI) tools can help identify and address potential biases within the credit scoring models more effectively.

Infrastructure readiness also plays a crucial role. Organisations need robust technological systems capable of securely handling vast volumes of alternative data, integrating it with traditional credit data, and supporting advanced analytics like machine learning. Scalable and secure cloud-based solutions often provide the flexibility required to manage growing data demands effectively.

Regulatory Compliance in Credit Risk Scoring

Regulatory compliance in credit risk scoring is essential to protect consumer privacy, ensure fairness, and maintain transparency in data usage.

Key regulations include GDPR in Europe, the CCPA, the Lei Geral de Proteção de Dados (LGPD), and local credit bureau rules. These frameworks set strict guidelines on data collection, processing, sharing, and user consent.

Adhering to these rules ensures individuals' personal data is handled responsibly, reducing risks of misuse and identity theft. It promotes fairness by preventing discriminatory credit decisions and fosters transparency through clear communication about data practices. Institutions must adhere to these regulations to build trust with customers and avoid legal penalties.

Credolab exemplifies compliance with a privacy-first methodology. It rigorously collects only anonymised, non-personally identifiable metadata with explicit user consent. This approach complies fully with GDPR, CCPA and the Lei Geral de Proteção de Dados (LGPD). Credolab’s transparent data usage policies empower consumers by respecting their privacy rights while enabling more accurate credit risk assessment.

By prioritising regulatory compliance, Credolab supports ethical credit scoring that meets evolving legal demands and protects consumer interests, making it a trusted partner for financial institutions aiming to adopt alternative credit data responsibly.

Understanding the Types of Credit Risk and Scoring Factors

The types of credit risk primarily involve two key types: default risk and concentration risk.

Default risk is the possibility that a borrower will fail to meet their payment obligations, either by missing payments or defaulting entirely. This risk directly affects lenders by causing financial losses when loans are not repaid. It is the most common type of credit risk evaluated in lending decisions.

Concentration risk occurs when a lender’s portfolio has a significant portion tied to a specific individual borrower or a small group. This lack of diversification increases vulnerability, as financial stress impacting those borrowers can lead to substantial losses for the lender. Focusing on diversification is therefore essential to manage concentration risk effectively, especially when concerning individual borrowers.

Key scoring factors help assess these risks to predict repayment behaviour accurately. Payment history is crucial as it tracks timely repayments and any delinquencies, reflecting past borrower reliability.

Behavioural data such as spending patterns, credit utilisation, and repayment trends provide deeper insights into a borrower’s financial discipline. While digital device data, including device type, IP addresses, and geolocation, assists in verifying identity and detecting potential fraud, adding robustness to credit scoring models.

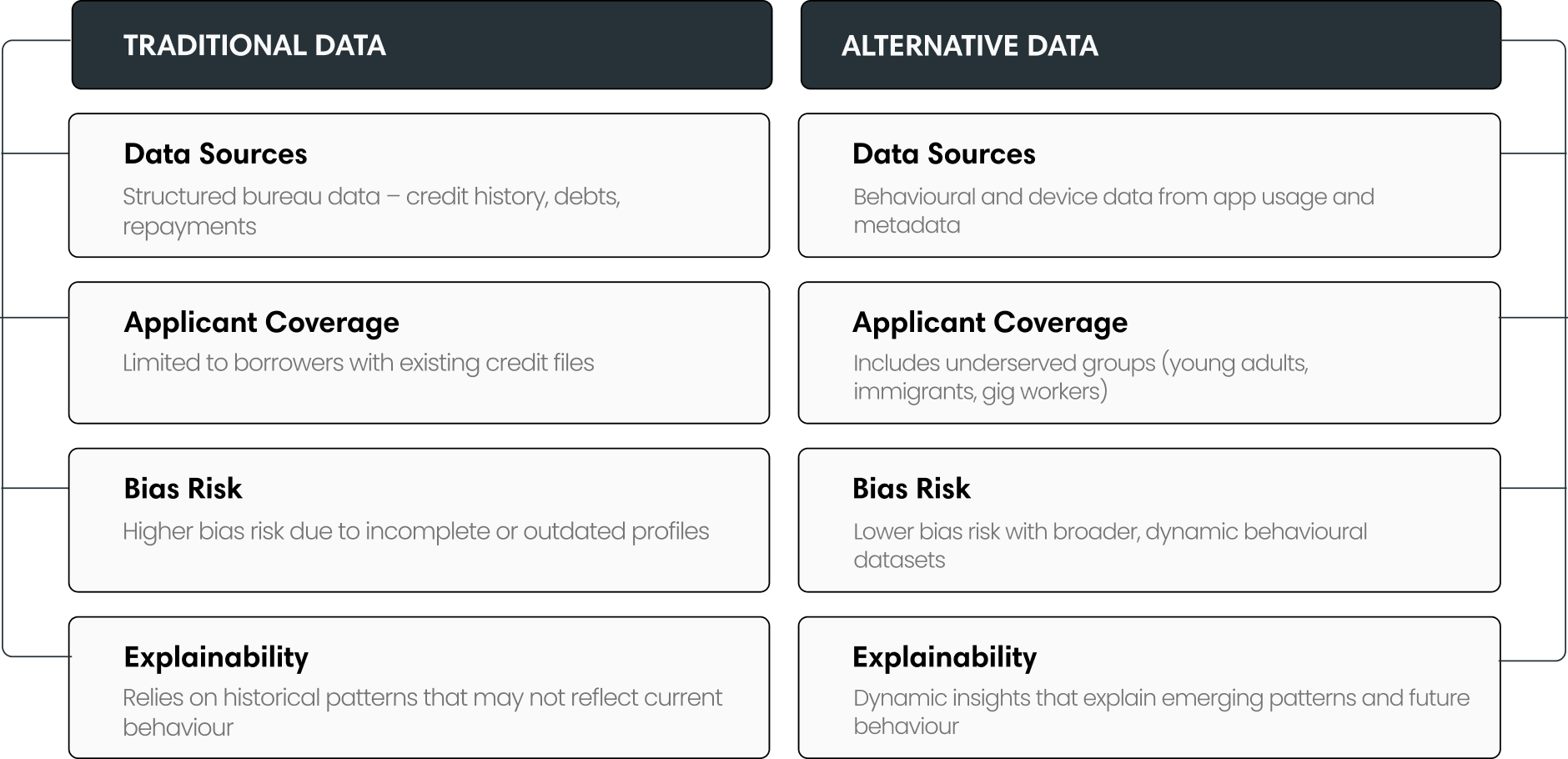

Traditional vs Alternative Credit Risk Scoring Models

Traditional credit risk scoring models rely primarily on structured data from credit bureaus. This includes credit history, loan repayment records, outstanding debts, and public records.

These models provide a reliable evaluation of creditworthiness based on established financial behaviours. However, their scope is limited to individuals with existing credit files, effectively excluding thin-file or no-file applicants. Decision speed in traditional scoring varies but often involves batch processing, which can delay outcomes.

Alternative credit risk scoring models incorporate a broader range of various alternative data sources from behavioural biometrics to app usage data.

By utilising real-time or near-real-time data, alternative scoring methods enable faster, more dynamic decision-making. This agility is ideal for digital lending environments that require quick loan approvals. Scalability is enhanced as models can process vast, diverse datasets, adapting to new data streams and borrower behaviours.

Applicant coverage is a key differentiator. Traditional models predominantly serve borrowers with established credit histories.

In contrast, alternative models extend financial services to underserved populations such as young adults, immigrants, gig economy workers, and those in emerging markets. This inclusivity broadens the lending market and promotes financial inclusion.

The Credolab’s Credit Risk Scoring Process Explained

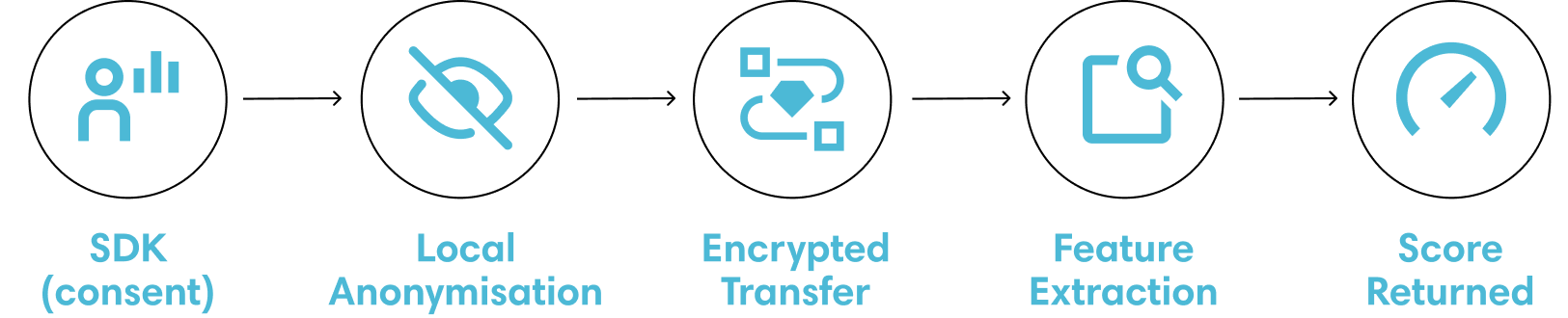

Credolab’s credit risk scoring process begins with their proprietary SDK embedded in lenders’ apps or online forms. This SDK collects only anonymised, first-party behavioural and device metadata from users who have given explicit consent. No personal identifying information (PII) is accessed or stored, ensuring full privacy compliance.

The collected data includes device signals, app ownership and installation patterns, network details, and application form behavioural data which are encrypted and securely transmitted to Credolab’s servers. This metadata is then processed through advanced machine learning models that analyse over 11 million features to identify behavioural patterns linked to credit risk.

The machine learning scoring engine continuously refines its accuracy by training on repayment data from lenders. The final credit risk score is delivered back to lenders in real time, enabling rapid, informed lending decisions.

Credolab’s privacy-first methodology ensures compliance with GDPR, CCPA, LGPD, and other global privacy regulations. The company collects privacy-consented, anonymised, non-PII metadata from users, guaranteeing that personal data is never accessed or processed.

Its scalable infrastructure supports high-volume processing, making it suitable for lenders of all sizes. It leverages cloud-based architecture and modular SDKs that allow seamless integration and rapid handling of large data volumes without performance degradation.

This approach combines secure, consent and permission-based alternative data collection with powerful risk analytics, improving credit access while protecting user privacy and reducing risk for lenders.

How AI/Machine Learning is Improving Credit Risk Scoring

AI and machine learning have transformed credit risk scoring by enabling faster, more accurate, and adaptive assessments that go beyond traditional data and methods.

These technologies leverage vast and varied data sources, uncover complex patterns, and continually learn from new information. However, with increasing model complexity comes the challenge of model interpretability.

AI in Credit Scoring and Avoiding the “Black Box Effect”

AI-powered credit scoring has transformed lending by enhancing predictive accuracy. However, complex models often face the “black box” problem or the inherent inexplicability of AI models, where the decision-making process is opaque and difficult to interpret.

This lack of transparency poses challenges in regulated industries that require clear explanations for credit decisions. Although techniques like SHAP values and feature importance can help interpret complex models, these solutions are difficult to implement and typically require highly advanced data science expertise.

To address this, some alternative credit scoring platforms use a data modelling process based on machine learning techniques that prioritise statistical explainability from the outset, ensuring clarity and transparency in credit decision-making.

These tools help lenders understand which variables influenced a score, ensuring compliance and fostering trust among consumers and regulators. Therefore creating a transparent framework for ethical and explainable decision-making.

Leveraging Machine Learning for Smarter Credit Risk Models

Machine learning enables the creation of adaptive, data-driven credit risk models that surpass traditional static methods.

Machine learning algorithms analyse large and diverse datasets, including alternative data sources, to detect subtle and non-linear patterns linked to fraudulent or delinquent behaviours.

This improves accuracy and allows models to evolve quickly as borrower behaviour changes. Furthermore, machine learning accelerates insights by automating data processing, enhancing risk prediction speed, and enabling personalised scoring based on individual behaviour rather than broad categories.

Together, these advances facilitate smarter, faster, and more inclusive lending decisions while maintaining fairness and regulatory compliance.

Credit Risk Score Calculation Example

Calculating a credit risk score involves combining various borrower attributes into a numerical score that predicts the likelihood of default. A traditional, linear scoring process usually includes these steps:

- Data Collection: Gather key borrower information such as payment history, outstanding debt, income level, credit utilisation, and recent credit enquiries.

- Assigning Weights: Assign a weight or score based on its predictive power for each attribute. For instance, timely payment history might have a high positive weight, while high credit utilisation would have a negative weight.

- Calculating Sub-scores: Multiply each attribute’s value by its corresponding weight to calculate sub-scores.

- Summing Scores: Add all sub-scores to get a total credit risk score.

- Interpreting Score: Scores fall within a range (e.g., 300 to 850). Higher scores indicate lower risk, while lower scores indicate higher risk of default.

For example, if the payment history weight is +50 for good history and the borrower has this, they earn +50 points; if credit utilisation has a weight of -30 and the borrower has high utilisation, they lose 30 points.

Modern machine learning models like Credolab's are more complex and analyse thousands of non-linear data points simultaneously.

These points sum to the final credit score guiding lenders on creditworthiness. This scoring process enables lenders to rank applicants objectively, set credit limits, and price loans according to risk.

How Credit Risk Analytics Platforms Support Risk Teams

Credit risk analytics platforms help to automate credit risk detection, assessment, and scoring through advanced data analysis and predictive models.

Key features include interactive dashboards that provide real-time insights into credit portfolio performance and risk indicators. Real-time scoring capabilities enable instantaneous evaluation of new credit applications or changes in borrower profiles, helping teams make fast, informed decisions.

Meanwhile, a credit risk management platform integrates diverse data sources, seamlessly layering traditional financial information with alternative data to provide a comprehensive view of borrower risk.

Furthermore, advanced credit risk management tools generate detailed, customisable reports for monitoring risk trends, portfolio health, and compliance with regulatory standards.

Automation reduces manual errors and workloads by streamlining credit risk workflows such as application processing, score updates, and alert generation for emerging risks. This also supports compliance by maintaining audit trails, enforcing consistent risk policies, and facilitating regulatory reporting requirements.

Benefits of Using Alternative Data in Credit Risk Scoring

Alternative data offers several advantages that enhance credit risk scoring. It increases access by enabling lenders to evaluate individuals who lack extensive traditional credit histories, thus expanding credit opportunities for students, young professionals, gig-economy workers, small business owners and other underserved or unbanked populations.

Real-time scoring based on fresh data instead of historical data is another benefit, as alternative data reflects current financial behaviour, allowing for instant and dynamic credit assessments. This timeliness helps lenders respond better to changes in a borrower’s creditworthiness.

Additionally, using alternative data reduces bias found in traditional credit models driven heavily by historical credit information. By incorporating diverse data sources such as utility payments, mobile phone usage, and behavioural signals, scoring becomes more inclusive and fair, not to mention accurate.

Alternative data also helps detect fraud patterns and create more complete borrower profiles, enhancing risk visibility. This reduces the risk of default and contributes to portfolio quality. Moreover, lenders can tailor their products more effectively by understanding nuanced customer behaviours, leading to better customer satisfaction and retention.

Increase Accessibility

Enables lenders to score thin-file and underserved customers.

Ensures Timeliness

Uses real-time data for instant, dynamic credit assessments.

Guarantee Inclusivity and Fairness

Reduces bias with diverse, non-traditional data sources.

Enhance Risk Visibility

Reveals behavioural patterns and builds more complete profiles.

Reduce Risk of Default

Improves predictiveness and strengthens portfolio quality.

Improve Customer Satisfaction and Retention

Enables tailored products through nuanced behavioural insights.

Best Practices for Effective Credit Risk Scoring and Management

Effective credit risk scoring and management are critical for financial institutions to reduce loan defaults and maintain portfolio health. Here are some practical tips to optimise these processes:

Define Clear Objectives

Set specific goals to guide model design, data selection, and workflows.

Use Quality Data

Incorporate diverse, reliable data sources and update them regularly.

Adopt Advanced Analytics

Leverage ML and XAI for adaptive, transparent, and compliant risk models.

Implement Real-Time Scoring

Use real-time data streams for dynamic assessments and timely decisions.

Ensure Transparency

Apply XAI to avoid black-box models and strengthen regulatory trust.

Foster Strong Governance

Establish clear roles, oversight, and independent reviews for accountability.

Use Scenario Analysis and Stress Testing

Simulate adverse conditions to identify vulnerabilities and adjust strategy.

Promote Continuous Improvement

Monitor model performance and refine practices to stay aligned with trends.

- Define Clear Objectives: Establish specific goals for credit and risk management, such as improving accuracy, reducing non-performing loans, or enhancing inclusion. Well-defined objectives guide model design, data selection, and workflow setup. Clear objectives also facilitate alignment across teams and support measurable performance tracking.

- Use Quality Data: Incorporate diverse and reliable data sources, including traditional credit histories and alternative data like utility payments or behavioural indicators. Regularly evaluate and update data to maintain accuracy and relevance. Continuously monitoring data quality ensures models remain robust against changing borrower behaviours.

- Adopt Advanced Analytics: Leverage machine learning and AI to create adaptive, nuanced risk models that capture complex borrower behaviour and non-linear relationships. Ensure models are regularly validated and recalibrated using recent data. Incorporating XAI enhances model transparency and regulatory compliance.

- Implement Real-Time Scoring: Enable dynamic risk assessment by integrating real-time data streams. This allows quick responses to changes in borrower status, market conditions, or external events, improving risk mitigation. Real-time scoring also supports more personalised lending decisions based on current borrower profiles.

- Ensure Transparency: Avoid “black box” models by using XAI techniques that provide clear, interpretable credit decisions. Transparent models enhance regulatory compliance and build customer trust. Clear explanations also help in addressing customer disputes and improving communication.

- Foster Strong Governance: Implement robust governance frameworks with clear roles, responsibilities, and oversight for credit risk processes. Regular independent reviews and audit trails ensure consistency and accountability. Effective governance supports timely escalation of risks and policy enforcement.

- Use Scenario Analysis and Stress Testing: Simulate adverse economic scenarios to evaluate portfolio resilience and adjust risk strategies proactively. Stress testing helps identify vulnerabilities before they impact the portfolio, enabling pre-emptive corrective actions.

- Promote Continuous Improvement: Monitor model performance regularly, capture feedback, and update risk management practices to adapt to evolving market trends and regulatory changes. A culture of continuous learning improves risk prediction and keeps the institution competitive.

These enhancements ensure a comprehensive, reliable, and compliant credit risk management process suitable for today’s dynamic financial environment.

The Business Impact of Smarter Credit Risk Scoring

Smarter credit risk scoring powered by machine learning delivers substantial business value across lending operations. These values include:

- Higher approval rates arising as models analyse diverse data, including alternative sources, enabling credit access for previously underserved or “thin-file” applicants. This expansion of borrower reach grows lender market share while maintaining portfolio quality.

- Lower default rates resulting from more accurate risk segmentation, where machine learning models capture complex borrower behaviours and shifting economic conditions dynamically. By identifying risk patterns early, lenders can adjust loan terms, pricing, or decline high-risk applications, reducing losses and improving profitability.

- Improved risk segmentation enhancing portfolio performance by grouping borrowers more precisely according to credit risk bands. This allows tailored credit limits, interest rates, and collections strategies aligned to the borrower’s risk profile, optimising capital allocation.

- Machine learning also supports fairer scoring by mitigating traditional biases inherent in traditional credit scoring. By incorporating non-traditional behavioural and alternative financial data, lenders evaluate creditworthiness more inclusively, promoting financial inclusion and regulatory compliance.

Key Takeaways

- Clear objectives are essential to guide credit risk management strategies and measure success effectively.

- High-quality, diverse data improves model accuracy and relevance over time.

- Advanced analytics like machine learning enable more precise and adaptive risk models.

- Real-time scoring supports timely, personalised credit decisions.

- Transparent models build trust and ensure regulatory compliance.

- Strong governance and clear accountability maintain consistent risk management.

- Continuous improvement fosters resilience and responsiveness to market and regulatory changes.

These best practices collectively strengthen credit risk scoring and management, leading to more accurate decisions, reduced defaults, and greater financial inclusion in today's dynamic lending environment.

How Can Credolab Help with Credit Risk Assessment?

Credolab helps financial institutions enhance credit risk assessment through seamless SDK integration, advanced alternative data analytics, and privacy-first scoring models.

Its lightweight SDKs for Android, iOS, and web are easy to embed with minimal impact on app or website performance, allowing quick deployment and real-time, in-session data capture. Credolab collects only privacy-consented, anonymised, non-PII behavioural metadata from users’ mobile devices and web interactions.

This data includes usage patterns, device settings, and UI gestures, which are processed through proprietary machine learning models. These models generate accurate, predictive risk scores that improve credit decisions even for applicants with limited traditional credit history.

Privacy and compliance are central to Credolab’s approach, ensuring adherence to GDPR, CCPA, LGPD, and other data protection regulations. Clients maintain full control over data collected, with user consent required before any information processing.

Credolab’s secure, scalable technology improves risk prediction and reduces default rates and also supports greater financial inclusion by providing lenders with deeper insights from alternative data sources.

Credolab in Action

Behavioural and device-based insights driving measurable credit outcomes.

Projected new approval rate

compared to your current approval baseline.

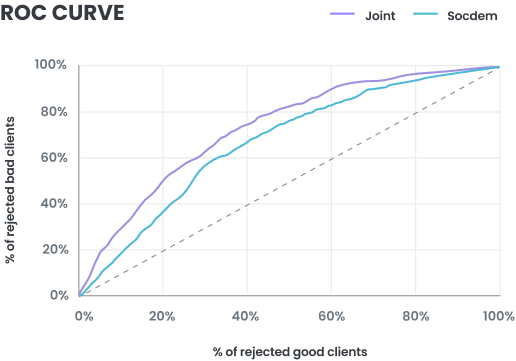

A leading digital lender integrated Credolab's behavioural metadata score to enhance early-stage risk assessment and expand safe approvals.

Consumer loans in Colombia

- Gini score 21.2

- Increased predictive power by 20%

- Improved false positive detection by rejecting 30%, including risk applicants

- Decreased bad rates by 6.67%

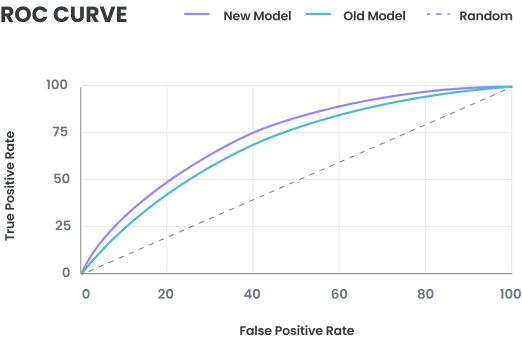

Neobank in The Philippines

- Gini 0.29 standalone

- Gini 0.35 with Credolab

- Gini 0.42 joint model

- Increased predictive power by 45%

- Decreased default rates by 50%

Conclusion

Effective credit risk assessment combines structured evaluation of borrower creditworthiness with continuous risk management to safeguard the ' financial stability of institutions.

Integrating traditional scorecards with alternative data and AI-powered models enables more precise and dynamic risk analysis. Privacy-conscious data collection and compliance with evolving regulations remain foundational.

Financial institutions that adapt to these advancements position themselves for sustainable growth and competitive advantage in a rapidly digitalising lending landscape.

FAQs

What is a credit risk analysis?

Credit risk analysis evaluates the likelihood that a borrower will default on debt obligations. It involves examining financial health, credit history, cash flows, and collateral quality to predict potential losses and ensure informed lending decisions.

What are the 5 credit risk assessments?

The five key credit risk assessments are Character (borrower's trustworthiness), Capacity (ability to repay), Capital (borrower's net worth), Collateral (assets securing the loan), and Conditions (economic and industry factors impacting repayment).

What is the process of credit risk management?

Credit risk management involves identifying, assessing, mitigating, monitoring, and controlling credit risks through policies and processes to minimise losses while supporting profitable lending.

What is the credit risk scoring model?

A credit risk scoring model uses statistical or machine learning methods to quantify borrower risk by analysing various financial and non-financial factors, producing a numerical score predicting default probability.

How does machine learning improve credit risk analysis?

Machine learning enhances credit risk analysis by detecting complex patterns, incorporating alternative data, adapting quickly to new information, and providing more accurate, dynamic, and inclusive risk predictions.

How to calculate credit risk score?

Credit risk scores are calculated by assigning weights to borrower attributes like payment history and debt levels, multiplying these by values, and summing for a total score indicating creditworthiness.