June 18, 2026

Credit Scoring

Lenders face a dual challenge: increasing approval rates while managing risk in a volatile economy.

As financial conditions shift rapidly, institutions must continue to grow without weakening their credit portfolios.

Balancing commercial targets with risk controls has become more difficult, especially in unpredictable markets.

Millions of people around the world are considered "credit invisible" or have thin credit files, making them ineligible for traditional credit products.

These include young adults, gig workers, and migrants who often lack formal financial histories but demonstrate strong financial responsibility.

This segment remains largely untapped and presents a major opportunity for growth and financial inclusion.

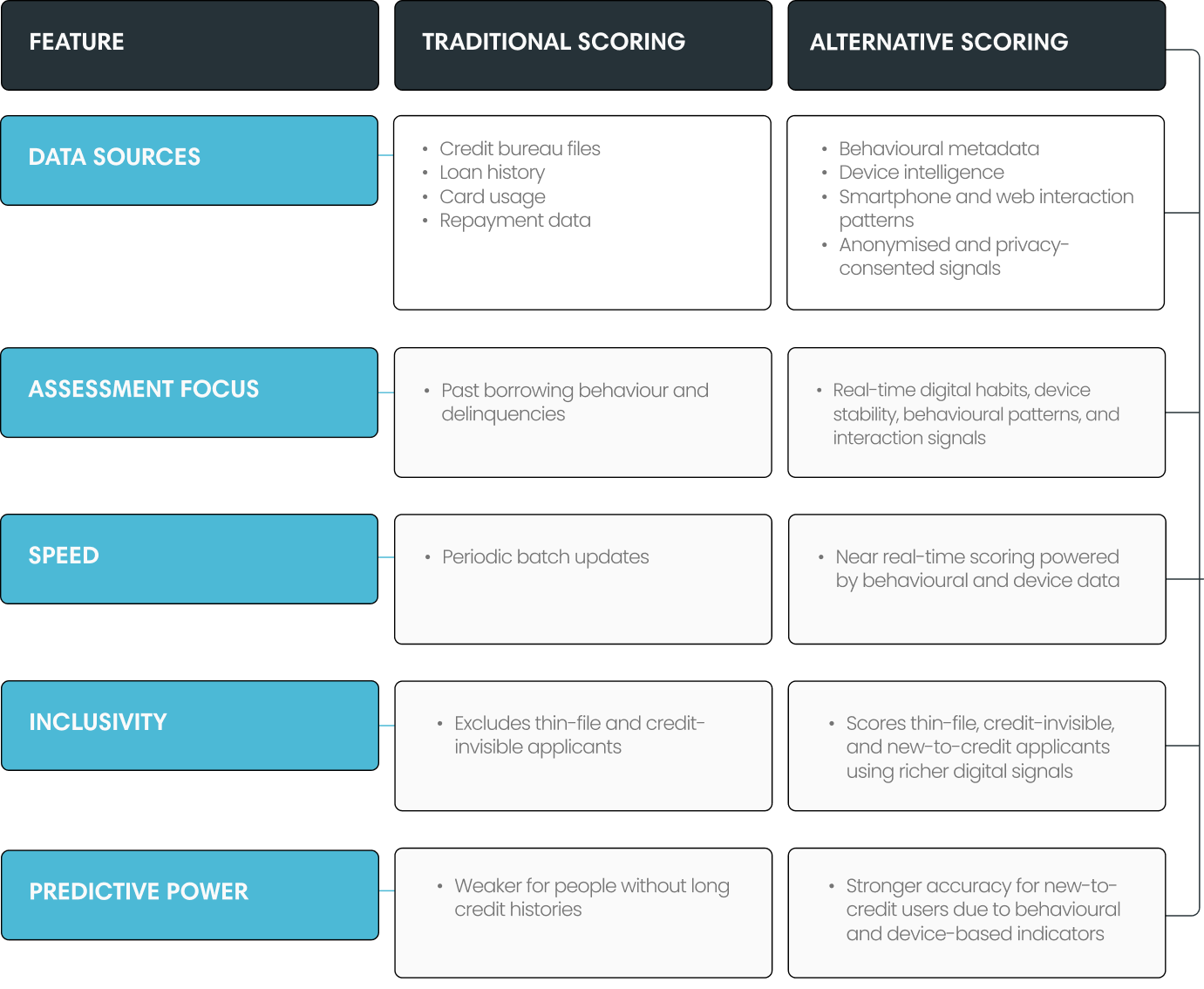

Traditional credit scoring systems depend almost entirely on formal banking and historical credit data.

This outdated approach overlooks many financially active individuals who operate outside conventional credit frameworks.

As a result, lenders routinely reject applicants who may in fact be low-risk and creditworthy.

Alternative credit scoring addresses this disconnect by analysing data beyond traditional credit reports. These include utility payments, mobile usage, rental history, behavioural data, etc.

These additional indicators provide a clearer view of an applicant’s financial behaviour and risk profile.

With the support of machine learning (ML), lenders can make faster, fairer, and more accurate decisions at scale.

Alternative credit scoring assesses creditworthiness using non-traditional data instead of relying only on credit bureau records.

It considers broader transactional signals to estimate a person's likelihood of repayment.

Often powered by ML, it helps lenders evaluate applicants with little or no formal credit history.

Alternative credit scoring forms a more holistic, real-time understanding of each applicant by incorporating multiple data sources, including financial, digital and behavioural data that traditional models do not capture. This enables lenders to improve coverage and decision accuracy, approving more customers while maintaining controlled risk levels.

Here are the types of signals referred to when talking about alternative data. They are already widely used in production and form the backbone of modern, more inclusive credit scoring models.

Standard alternative data refers to non-traditional yet widely accepted data sources that describe how people earn, spend, and behave digitally.

These sources are already being used in production by leading alternative credit scoring providers to complement bureau and banking data.

Transactional data captures real economy behaviour such as e-commerce purchases, utility bill payments and telco top-up histories.

Patterns in frequency, regularity and arrears provide strong signals about affordability, stability and willingness to pay.

Device metadata focuses on how a person configures and uses their smartphone, including app ownership, installation patterns and device preferences.

Signals such as contacts saving patterns, calendar usage and reminders creation can correlate with organisation, reliability and financial discipline.

Behavioural metadata records how users interact with their devices and apps, such as keystroke dynamics and in-app navigation patterns.

When combined with behavioural biometrics, it can reveal behavioural consistency, digital confidence, decision-making patterns, and anomalies that may indicate increased fraud risk or influence potential repayment challenges.

Together, these standard alternative data categories give lenders a richer, near-real-time view of customers than traditional files alone.

They supply the raw material that ML models need in order to build more inclusive and predictive credit scores.

Credolab’s innovation lies in its use of device and behavioural metadata to assess credit risk without collecting personal information.

Credolab uses behavioural biometrics to understand how users behave and how they interact with their device, not who they are. It collects zero personal data and works exclusively with non-personally identifiable information (non-PII).

Anonymised metadata from smartphones and web interactions—such as typing speed, swipe patterns, and time taken to complete a form—provides predictive signals of repayment likelihood and digital behavioural patterns.

For instance, consistent typing speed and smooth swipe gestures often indicate consistent interaction habits and attention to detail. Both of these correlate with reliable repayment patterns.

Similarly, users who complete application forms without prolonged hesitation typically exhibit greater digital confidence and decisiveness, which Credolab identifies as indicators of lower credit risk.

Credolab’s insights reveal that structured device usage and behavioural stability—such as regular interaction with calendar apps or consistent app installation habits—tend to align with more financially disciplined behaviour.

In contrast, irregular input patterns, erratic interaction speeds or minimal engagement with organisational tools may serve as red flags and signal higher-risk behavioural profiles.

Without accessing any personal content, this type of metadata allows lenders to build accurate and inclusive risk profiles, particularly for applicants without traditional credit histories.

Alternative credit scoring enables lenders to approve more applicants, including those who are traditionally excluded due to thin or nonexistent credit files.

By using behavioural and transactional signals, lenders can assess creditworthiness more accurately and reach untapped segments with confidence.

ML models built on alternative data detect risk patterns earlier than traditional systems.

Changes in user behaviour—such as erratic device interaction or form completion delays—can indicate instability in digital behaviour before a missed payment occurs. It allows for timely interventions.

Relying solely on static bureau data is no longer sufficient in today’s fast-moving economy.

Alternative credit scoring offers real-time, adaptable insights that help lenders adjust risk strategies in response to behavioural shifts.

This ensures long-term competitiveness and better preparedness for market volatility.

Alternative credit scoring transforms raw alternative data into reliable lending alternative credit decisioning through a simple, four-step ML process.

The journey begins with consented, privacy-first collection of alternative data from sources such as device signals, app interaction patterns, telecom or utility information, and device and behavioural metadata.

Data is anonymised or pseudonymised, with clear disclosures so customers understand what is being used and for what purpose.

Next, ML algorithms, supported by artificial intelligence (AI) techniques where appropriate, scan the data to detect patterns and relationships.

They convert raw signals like typing speed, app usage or interaction timing into structured variables that can be analysed consistently.

These variables are used to train predictive models that learn from past loans, helping the system recognise which behaviours are commonly associated with successful repayment and which are associated with missed payments or higher default risk.

Models are validated, monitored and recalibrated to prevent bias and to ensure they remain accurate over time.

Finally, the output is translated into scores, risk bands and recommended actions that business teams can easily understand.

Lenders can use these insights to approve or decline applications, set limits, price risk and design proactive customer strategies, all while keeping the process explainable and auditable.

Begin by clearly outlining the goals for using alternative data for credit scoring.

Are you trying to increase approval rates, improve risk prediction, or expand into new customer segments?

Having a defined objective ensures the solution aligns with your credit strategy and risk appetite.

Deciding between building in-house or buying from a specialist provider is a key strategic choice.

Most lenders opt for external partners due to the technical complexity, time and compliance hurdles involved in building alternative scoring solutions from scratch.

Choosing the right partner means looking beyond the technology—data quality, explainability, integration support and privacy safeguards are all critical.

Once the partner and data sources are selected, integration with your existing systems is the next step.

Begin with a test or shadow scoring phase to validate model performance, benchmark outcomes and fine-tune thresholds.

This allows risk teams to gain confidence before moving to live production.

Ongoing model monitoring is essential to ensure accuracy and fairness over time.

Track outcomes, adjust to economic shifts and retrain models as new data becomes available. This iterative approach ensures long-term reliability and continuous improvement.

Ethical design and strong governance are what make modern alternative credit scoring trustworthy for regulators, lenders and end customers.

Regulatory compliance makes sure that the collection and processing of alternative data comply with global data protection laws. These include:

These frameworks govern how lenders collect, process and store data, and they protect users’ rights to transparency, access and deletion.

The updated Google Play Personal Loans policy now blocks certain lending apps from accessing sensitive data permissions, such as:

This restricts access to certain device signals, which can affect some scoring models.

Credolab takes a compliance-first approach. Its SDK has never relied on restricted permissions and maintains strong performance by using only approved, stable device and behavioural signals drawn from a much larger set of engineered features that remain unaffected by the Google Play policy updates.

Privacy by design is central, meaning data protection is built into the product from the start rather than added later.

Alternative scoring should rely on privacy-consented, anonymised metadata instead of raw personal content.

It minimises what is collected to what is strictly necessary for risk assessment. Strong encryption, access controls and secure development practices then ensure that this metadata is safeguarded throughout its lifecycle.

Fairness requires robust model validation to avoid reinforcing historical or demographic bias.

Lenders should test model performance across different groups, monitor for drift, and use explainability tools to understand which features drive outcomes.

Regular reviews, backtesting, and governance committees help ensure that alternative credit scores remain accurate, transparent, and non-discriminatory over time.

The future of alternative credit data scoring lies in the fusion of diverse data types—transactional, behavioural, and device-based—analysed through advanced ML and AI.

Financial institutions are increasingly adopting these models to gain deeper insights into borrower behaviour, especially in real time.

Behavioural biometrics is set to become the core of next-generation risk assessment.

It offers highly predictive, privacy-respecting insights that traditional methods cannot provide.

As this space evolves, compliance with global regulations will remain essential to ensure responsible and ethical use of alternative data.

Alternative credit scoring is more than just a tool—it represents a necessary evolution in how the financial system assesses trust.

By moving towards fairer, more inclusive, and efficient models, lenders can reshape global access to credit while maintaining accountability and transparency.

Alternative credit scoring is now a proven way for lenders to achieve better portfolio performance while managing risk responsibly.

By using richer data and ML, it delivers stronger predictive power, fewer bad loans, and more precise pricing.

Lenders gain practical advantages at every stage of the credit lifecycle. They can approve more of the right customers, spot early warning signs sooner, and optimise collections with data-led insights.

Because alternative credit scoring updates with fresh behavioural and device signals, risk models stay resilient in changing economic conditions.

This agility helps safeguard margins and capital when traditional indicators become less reliable.

At the same time, alternative credit scoring opens the door to borrowers who were previously invisible to the financial system.

People with thin credit files or no formal credit history can now be assessed based on how they use their devices and manage their digital habits.

In this sense, alternative scoring is not a niche add-on but a necessary evolution of modern lending. It allows growth, resilience, and inclusion to reinforce one another.

Lenders who embrace this shift today will be better positioned to make every decision the right one tomorrow.

Alternative credit scoring is a way of assessing a borrower’s risk using non-traditional data rather than relying only on credit bureau records.

It combines information such as transactions, device usage and behavioural patterns to estimate repayment likelihood.

This helps lenders approve more good customers, especially those with thin files.

Alternative credit refers to lending that relies on broader, non-traditional information to evaluate applicants, not just long-standing bank histories.

It uses signals such as digital payments, rent, utilities and device metadata to understand real financial behaviour accurately.

This approach supports fairer access to credit for underserved customers worldwide.

The four R’s of credit scoring commonly refer to Risk, Response, Retention and Revenue in many teaching frameworks today.

They summarise how lenders think about lending decisions over time.

Risk covers the probability of default, Response captures customer reactions, Retention focuses on keeping good borrowers, and Revenue reflects income generated overall.

The three C’s of credit usually mean Character, Capacity and Capital, sometimes with Collateral treated as part of Capital in practice.

Character reflects a borrower’s reputation and past behaviour. Capacity describes the ability to repay from income reliably, while Capital represents assets or savings that provide extra security for lenders overall.