March 24, 2022

Fraud

Credit risk modelling refers to the use of statistical and machine learning (ML) techniques to estimate key risk parameters, including the probability of default (PD), loss given default (LGD), and exposure at default (EAD). These metrics underpin expected loss calculations and inform pricing, credit limits, provisioning, and capital allocation decisions.

For lenders, accurate credit risk management models are critical for robust underwriting, continuous portfolio monitoring, regulatory compliance with IFRS 9 and Basel III frameworks, and achieving risk-adjusted returns.

In 2026, credit risk modelling is evolving rapidly as new technologies and regulatory expectations reshape the landscape. The adoption of artificial intelligence (AI) and ML continues to grow, while the EU AI Act is introducing greater scrutiny around model governance. At the same time, lenders are increasingly turning to alternative data to assess thin-file borrowers and manage risk in more volatile economic conditions.

This guide outlines core model types, development and validation processes, optimisation approaches, and how Credolab behavioural data can enhance model performance. It also highlights practical considerations for implementation, governance, and ongoing monitoring to ensure reliability and regulatory alignment in practice.

Credit risk modelling is the process of quantifying the likelihood and impact of borrower default using statistical and ML techniques. The core framework relies on three parameters: PD, LGD, and EAD. These inputs combine to estimate expected credit loss (ECL) through a standard formula.

In practice, lenders apply these models to AI credit scoring and scorecards, portfolio risk assessment, pricing, and provisioning under IFRS 9, as well as regulatory capital calculations under Basel III frameworks.

Consistent estimation improves decision making, risk segmentation, and capital efficiency, enabling lenders to balance growth with prudent risk management across economic cycles. It also supports transparent governance, model validation, and ongoing monitoring of credit performance metrics.

Credit risk modelling is shaped by global regulatory and accounting frameworks, particularly Basel standards and IFRS 9. These frameworks define how lenders estimate risk, calculate capital requirements, and recognise expected credit losses. However, they are not applied in exactly the same way across every market.

Although Basel and IFRS 9 are widely recognised as global standards, adoption varies by country and region. Some jurisdictions have fully implemented Basel III, while others continue to rely on Basel II or are still transitioning towards updated requirements. Similarly, while IFRS 9 is widely used for expected credit loss provisioning, some markets follow local accounting standards or alternative frameworks, such as CECL under US GAAP in the United States.

This means lenders need to consider both global principles and local regulatory requirements when developing credit risk models. A model that works well in one jurisdiction may need adjustments in another due to differences in capital rules, provisioning standards, supervisory expectations, or implementation timelines.

Different credit risk models support different decisions across the lending lifecycle. Some help lenders assess new applicants, while others estimate default risk, post-default losses, or more complex patterns in borrower behaviour. The key is to align each model with the decision it is meant to support. That could mean improving approvals, strengthening provisioning, refining pricing, or managing portfolio risk more effectively.

Application scorecards are used for credit approval and initial risk assessment. They typically rely on logistic regression, combined with Weight of Evidence (WoE) and Information Value (IV) binning, to transform variables and classify borrowers into good or bad risk categories in a consistent and interpretable manner.

PD models estimate the likelihood of borrower default. Common approaches include binary logistic regression and survival analysis for time-to-default estimation. Models are calibrated as point-in-time (PIT) or through-the-cycle (TTC), depending on economic sensitivity.

LGD and EAD models quantify post-default outcomes. These are typically developed using regression techniques or Tobit models to estimate recovery rates and outstanding exposure at the time of default.

Advanced approaches use ML techniques such as decision trees, random forest, gradient boosting, and neural networks to capture complex, non-linear relationships and enhance predictive accuracy. These models can be useful where lenders need to identify risk patterns that traditional approaches may miss, but they also require strong governance, monitoring, and explainability controls.

Most credit risk models follow a similar development path. The steps below show how models move from raw data to practical decision tools.

Prepare the data so the model reflects real risk, not data issues. Poor data quality can distort risk signals and lead to inconsistent decisions. This includes fixing missing values, treating outliers, and aligning formats across sources. Segment the portfolio where risk behaves differently, so the model captures meaningful patterns from the start.

Select variables that support clear and reliable decisions, not just statistical performance. If a variable cannot be explained or trusted, it becomes difficult to mause in practice. Techniques such as IV, correlation analysis, monotonicity checks, and the Variance Inflation Factor (VIF) help identify variables that are both predictive and stable.

Transform inputs to make risk patterns easier to interpret and more consistent over time. Without this step, models may rely on unstable or hard-to-explain relationships. Binning and WoE are commonly used to create clearer groupings and improve interpretability. This strengthens both model performance and governance.

Fit the model so it produces outputs that are not only accurate, but usable in real decisions. A model that performs well statistically but cannot be applied consistently creates operational risk. Logistic regression is commonly used due to its stability and interpretability, though other methods may be applied. Calibration ensures outputs are aligned with the decision context.

Set decision rules that translate model outputs into real actions. Cut-offs, overrides, and policy thresholds directly influence approvals, risk levels, and portfolio performance. Once deployed, monitor the model regularly. This helps ensure it remains aligned with portfolio behaviour and changing conditions, and signals when recalibration is needed.

Before relying on any credit risk model, it is important to understand how well it performs in practice. Performance metrics help assess whether the model is ranking risk correctly, producing reliable estimates, and remaining stable over time. Together, these measures provide a clear view of how effectively the model is supporting credit decisions.

Discrimination shows how well the model separates higher-risk borrowers from lower-risk ones. In practical terms, it answers whether the model is identifying risk early enough.

Metrics such as the Gini coefficient, KS statistic, AUC-ROC, and accuracy ratio are used to measure this. Strong discrimination supports better approvals, sharper pricing, and clearer risk segmentation.

Calibration checks whether predicted risk matches actual outcomes. If a segment is assigned a certain default level, observed defaults should broadly align.

Metrics such as the Hosmer-Lemeshow test and Brier score help evaluate this alignment across risk segments. Accurate probabilities are critical for pricing, provisioning, capital planning, and IFRS 9 ECL.

Stability looks at whether the model continues to perform consistently over time. Changes in data, borrower behaviour, or economic conditions can all affect performance.

The Population Stability Index (PSI) is commonly used to detect shifts in data distributions. Monitoring stability helps identify when recalibration or redevelopment is needed before performance deteriorates.

Building a model is only part of the process. It also needs to be tested, validated, and controlled over time to ensure it remains reliable and fit for purpose. Validation and governance help confirm that the model works in practice, meets regulatory expectations, and continues to support sound decision-making.

Validation focuses on how the model performs beyond development. Backtesting compares predictions with actual outcomes, while out-of-time and out-of-sample testing assess performance on unseen data. Benchmarking helps confirm whether results are strong enough, ensuring the model supports reliable decisions in practice.

Models must meet regulatory and accounting requirements. Under IFRS 9, this includes staging, significant increase in credit risk (SICR), and expected credit loss calculations. Basel standards require the use and validation of PD, LGD, and EAD, while the EU AI Act adds expectations around transparency, explainability, and governance.

Governance ensures the model remains controlled after deployment. This includes documentation, independent review, change management, and ongoing monitoring. Strong governance helps prevent model drift and inconsistent use, while keeping models aligned with risk policies and regulatory requirements.

Credit risk does not move in isolation. It changes with the economy, borrower behaviour, interest rates, employment conditions, and market stress. This is why forward-looking modelling has become central to modern credit risk management.

Under IFRS 9, expected credit loss is forward-looking, requiring lenders to estimate both 12-month and lifetime PD based on whether there has been a significant increase in credit risk. This approach ensures provisioning reflects how risk may evolve, not just current borrower conditions, supporting more realistic loss estimates and a clearer view of future portfolio risk.

Macro overlays link model outputs to broader economic conditions. Variables such as GDP, unemployment, inflation, and interest rates are used to adjust risk estimates across different scenarios. This helps ensure models remain relevant when conditions shift, allowing lenders to assess how the portfolio may perform under baseline, optimistic, and adverse environments.

Stress testing evaluates how the portfolio would perform under severe but plausible conditions, such as economic downturns or declining recoveries. It is often applied to parameters like LGD, where outcomes can worsen in stress scenarios. In practice, this supports capital planning, provisioning, and risk appetite decisions, helping lenders prepare for potential downside risk.

Credit risk model optimisation focuses on enhancing predictive accuracy, decision efficiency, and portfolio performance. This includes the use of dynamic cut-offs, which adjust approval thresholds in response to changing risk appetite, economic conditions, and observed portfolio behaviour. Champion–challenger testing is widely applied to compare incumbent models against new approaches, ensuring continuous improvement and selection of the most effective model.

Portfolio optimisation further aligns credit decisions with profitability, expected loss, pricing, and capital allocation objectives across segments. In addition, incorporating alternative and behavioural data can significantly improve credit risk optimisation model lift, often reflected in higher Gini coefficients, particularly for thin-file borrowers. This enables precise risk differentiation and stronger overall model performance.

Credolab, one of the alternative credit data scoring platforms, enhances credit risk modelling by introducing behavioural intelligence as low-correlation features. These complement traditional credit variables and strengthen PD models.

Using device metadata and behavioural interactions, such as application navigation patterns, typing behaviour, device consistency, and session characteristics, lenders gain additional predictive signals that are not captured in conventional bureau or financial data. These features are particularly valuable for thin-file or new-to-credit applicants, where traditional data is limited.

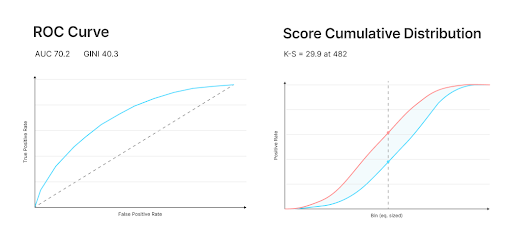

For one leading neobank in Southeast Asia, the challenge was to improve risk differentiation without disrupting the existing credit decisioning process. Instead of replacing the core scorecard, behavioural data was added as an additional layer through real-time Software Development Kit (SDK) and Application Programming Interface (API) scoring.

This allowed the lender to strengthen the model while keeping its existing infrastructure and decision workflow in place. The impact was visible at both model and business level. Model discrimination improved, with the Gini coefficient increasing from 32 to 43, while ROC AUC reached 70.2 and the KS statistic reached 29.9. In practical terms, this meant the lender was better able to separate higher-risk applicants from more creditworthy ones.

The business results followed the same pattern. Default rates fell from 26% to 18.3%, while approval rates increased from 8% to 9.6%. This showed that the enhanced model was not only reducing risk, but also helping the lender approve more suitable applicants with greater confidence.

Credit risk modelling continues to evolve alongside advances in data, regulatory expectations, and technology. Lenders that develop strong capabilities in estimating PD, LGD, and EAD are better positioned to manage risk and optimise portfolio performance. Robust scorecard development, combined with effective validation and governance practices, ensures that models remain accurate, stable, and compliant over time.

Simultaneously, frameworks such as IFRS 9 and Basel standards reinforce the need for forward-looking, transparent, and well-documented modelling approaches. The increasing use of alternative data and ML techniques further enhances predictive power, particularly for underserved or thin-file segments.

Lenders that successfully integrate these elements can achieve improved risk differentiation, better decision-making, and sustainable growth. They can also maintain a competitive advantage in an increasingly data-driven credit environment.

PD estimates the likelihood that a borrower will default, LGD measures the proportion of loss if default occurs, and EAD represents the outstanding amount at the time of default.

A credit risk scorecard is a statistical model, typically based on logistic regression, that assigns a score to borrowers to classify them into risk categories for credit decision-making.

12-month PD measures default risk over the next 12 months, while lifetime PD captures default risk over the entire remaining life of the loan, as required under IFRS 9.

Validation of credit risk models involves backtesting, out-of-time testing, benchmarking, and performance checks such as discrimination, calibration, and stability to ensure accuracy and reliability.

Macroeconomic variables such as GDP, unemployment, and interest rates are used in scenario analysis and forward-looking credit risk models to capture changing economic conditions and their impact on credit risk.

Credolab improves credit risk models by adding behavioural data as low-correlation features, enhancing predictive power, particularly for thin-file borrowers, and improving metrics such as Gini and KS.